This essay is not a ruling on permissibility, nor a rejection of Islamic legal principles. It is an attempt to examine how modern financial systems shape outcomes in practice, and why different contractual structures can converge in behavior when operating under the same constraints. The distinction in form remains real. The question explored here is how much of that distinction survives at the level of lived financial experience.

Islamic banking presents itself as an alternative to conventional finance. It replaces interest-based lending with Shariah-compliant contracts and emphasizes ethical structure over financial outcome.

In practice, however, the outcomes often look similar.

This raises a deeper question:

Is this similarity a failure of implementation, or a result of the system Islamic finance operates within?

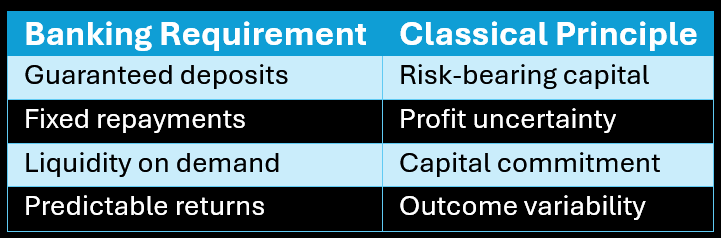

1. What Modern Banking Requires

Modern banking is not just a set of contracts. It is an integrated system with non-negotiable constraints.

Banks must:

- guarantee deposits

- provide liquidity on demand

- manage regulatory capital requirements

- produce stable and predictable returns

- minimize risk across their balance sheet

These are structural requirements. A bank that fails to meet them cannot function.

This creates a system built around:

- certainty over uncertainty

- guarantees over exposure

- predictability over variability

2. What Classical Islamic Finance Assumes

Classical Islamic commercial law developed in a different environment.

Its core financial structures include:

-

Mudarabah - capital and labor share profit and loss

-

Musharakah - partners share capital, risk, and return

These structures assume:

- profit is linked to risk

- capital is exposed to loss

- outcomes are uncertain

- returns cannot be guaranteed

The system is built around participation in real economic activity, not the management of financial certainty.

3. The Structural Collision

When Islamic finance enters the modern banking system, these two logics meet.

They are not easily reconciled.

These are not surface-level differences. They reflect opposing design principles.

4. How Convergence Happens

Faced with these constraints, Islamic finance adapts.

In practice:

- ownership becomes brief or symbolic

- risk exposure is minimized

- returns are fixed in advance

- contracts are structured to meet regulatory and liquidity demands

The result is a system where:

- form reflects Islamic contracts

- outcomes align with conventional finance

This is not accidental. It is a response to the environment.

5. The Critical Question

At this point, the discussion shifts.

The question is no longer:

Are specific contracts compliant?

It becomes:

Can a system built on uncertainty, risk sharing, and non-guaranteed returns operate inside a framework that requires guarantees, liquidity, and predictability?

6. Three Possible Positions

There are three ways to answer this.

A. Compatibility

Islamic banking works as intended. The differences in contract form are meaningful, even if outcomes appear similar.

B. Convergence

Islamic finance, when operating within modern banking constraints, will tend to converge with conventional outcomes. Differences remain at the level of form and procedure.

C. Structural Mismatch

The principles of classical Islamic finance require a different institutional structure altogether. A true alternative cannot be built within the existing banking system.

7. A Structural Reading

What we observe today suggests that convergence is not a failure of intent.

It is a consequence of operating within a system designed around:

- guaranteed deposits

- fixed repayment structures

- centralized risk management

- predictable financial outcomes

Under these conditions, financial products tend to move toward similar economic results, even when constructed differently.

This does not make the contracts identical. It does mean that their outcomes are shaped by the same constraints.

8. The Implication

If this reading holds, the discussion around Islamic finance changes.

The issue is no longer limited to contract compliance.

It extends to a deeper question:

Does the modern financial system allow for meaningful structural divergence, or does it absorb alternative models into its own logic?

9. Closing

Islamic finance today operates within the architecture of modern banking.

It adapts to that architecture, rather than replacing it.

Understanding this does not resolve every question. It clarifies where the tension comes from.

And it explains why different systems, built on different principles, often produce similar results.